We thought we would leverage this quarter’s update to include the most important questions investors have been asking, or should be pondering, along with our answers. If you have additional questions you would like us to address, feel free to send them along to us!

Is there a risk that stock markets have advanced too far, too fast, in recent years?

This is an important question that should be considered from several perspectives. If the current level of stock prices has already discounted all the current and future “good news,” then stock markets could be at risk. Let’s break this down.

Yes, the 37% rally from the April lows is astonishing, however one must consider that it came on the heels of a 20% decline in indexes, spurred by fears that tariffs would put an end to economic growth. Fears that – in hindsight – were misguided. Not surprisingly, for those of us who study “ugly math,” most of the ensuing rally (75% of it) was simply recovering from that 20% loss! Since the beginning of the year (a more logical viewpoint) US stocks have advanced 13%, while global stocks have returned 17%. Given year-to-date return equity returns and underlying earnings growth rates (particularly for the stocks you own), the stock market is not – at least yet – overvalued.

Since the AI-driven global bull market began in earnest in the autumn of 2023 (two years ago), global equity prices have advanced by 56%. Though this may seem like a surprisingly strong period for equities, it is in line with the first two years of past bull markets. Keep in mind that the first two years of a bull market are typically the strongest because investors at the bottom are often holding too much cash and too few stocks, creating heavy demand as the economy improves and markets recover. This set of factors creates tremendous demand for stocks and drives above average returns – which is what we have seen.

Given the healthy fundamentals of economic and corporate profit growth, as well as stock prices relative to earnings, stocks are not currently overvalued. However, as we will discuss, we are experiencing a significant shift in global economic policies, which could change this current healthy view of stock prices and valuations.

I’ve heard you discuss the possibility of the DOW reaching 100k – how is this possible?

We do think that DOW 100k is likely in the next five to six years. That may be hard to envision since the index is currently hovering around 46,000. However, one must consider that we are just two years into a new economic cycle – one that is being driven by the powerful forces of Artificial Intelligence (AI). Keep in mind that economic cycles typically last seven to nine years and bull markets coincide with these time periods. Moreover, AI has created a capital investment boom that surpasses anything we have ever witnessed, which we believe will create significantly higher productivity growth for the global economy and tailwinds for higher-than-normal stock price returns. When we make some conservative assumptions on future economic growth, corporate profits, productivity growth, and equity valuations and apply them to the DJIA, S&P 500, Nasdaq, and MSCI All World Index, we arrive at Dow 100k, Nasdaq 50k, and S&P 500 15k.

Unemployment seems to be rising in the US – does that increase the risk of a US recession and bear market?

In the US we are experiencing rising unemployment, which some, including the Federal Reserve, take as a sign of a weakening economy. Over 70% of the US economy is based on consumer spending, so levels of employment certainly factor into its health. Therefore, it makes sense that the Federal Reserve is reducing interest rates which is stimulative to jobs growth. However, what we find interesting is that, aside from the labor force decline, all else in the US economy remains healthy – GDP growth is around 3% and corporate profitability continues to beat expectations. It is quite possible that the unemployment levels are more a reflection of immigration policy and AI substituting “man for machine.” If this is the case, the Fed will want to be cautious about cutting rates too far. Doing so in a strong and resilient economy can create the risk of once again igniting inflation, which would be counter to the Fed’s mandate of stable prices.

The US administration’s domestic and foreign economic policies have been considered extreme – what are the implications for the US economy?

We describe the significant shift in US economic policy as the “New World Order.” The US economic policies of the last three decades made the US the most admired economy in the world and the US stock market the most “exceptional.” We believe that the current administration’s move towards protectionism, limited immigration, fiscal restraint, and trade will create headwinds for domestic economic and corporate profit growth. Fortunately, these headwinds can be somewhat counterbalanced by the fact that US companies are the primary driver of AI innovation and technology, which can help support economic growth and make our economy more productive. The wide disparity of tech stock performance versus the rest of the US stock market is a sign of where profit growth is strong...and where it isn’t. Growth in the tech sector, coupled with a boom in productivity growth and a more accommodative monetary policy, should create an economy that remains in growth mode – but perhaps not at the levels enjoyed over the previous three decades.

Why have foreign markets outperformed the US this year?

For the first time in over 15 years, foreign stocks are outperforming US indexes – and by a wide margin. Much of this is related to the “New World Order” of the US administration. The US global economic policies are significantly benefiting foreign economies and financial markets. As the US withdraws foreign funding and financial support, these regions are taking a page from “The Great American Playbook” by significantly increasing fiscal spending and easing monetary policy. Foreign economies are now gaining strength, and markets are reacting. This year alone foreign market performance has surpassed that of US market indexes, and we believe this will be the case for a number of years to come. Given that foreign markets have been neglected for many years, stocks are very undervalued and most global investors are extremely under-allocated. This combination of strong economic fundamentals, solid performance, and bargain stock prices is likely to create a buying spree in foreign stocks over the next few years. Hence our significant exposure to international stocks in your portfolio.

What are the best sectors to invest in the US? Overseas?

The US stock market is being led by only a few sectors for the reasons discussed above. Domestic growth is more limited than in the past, and the best profit growth is in only a handful of sectors which include AI tech, financials, and energy efficiency. Investors would be wise to focus on these areas, which include companies such as JP Morgan, Nvidia and GE Vernova. In overseas markets there is a broad-based rally that seems to include all sectors: from industrial companies like Siemens, to financials such as HSBC, and material companies such as Linde. Sector allocation is crucial to long-term performance.

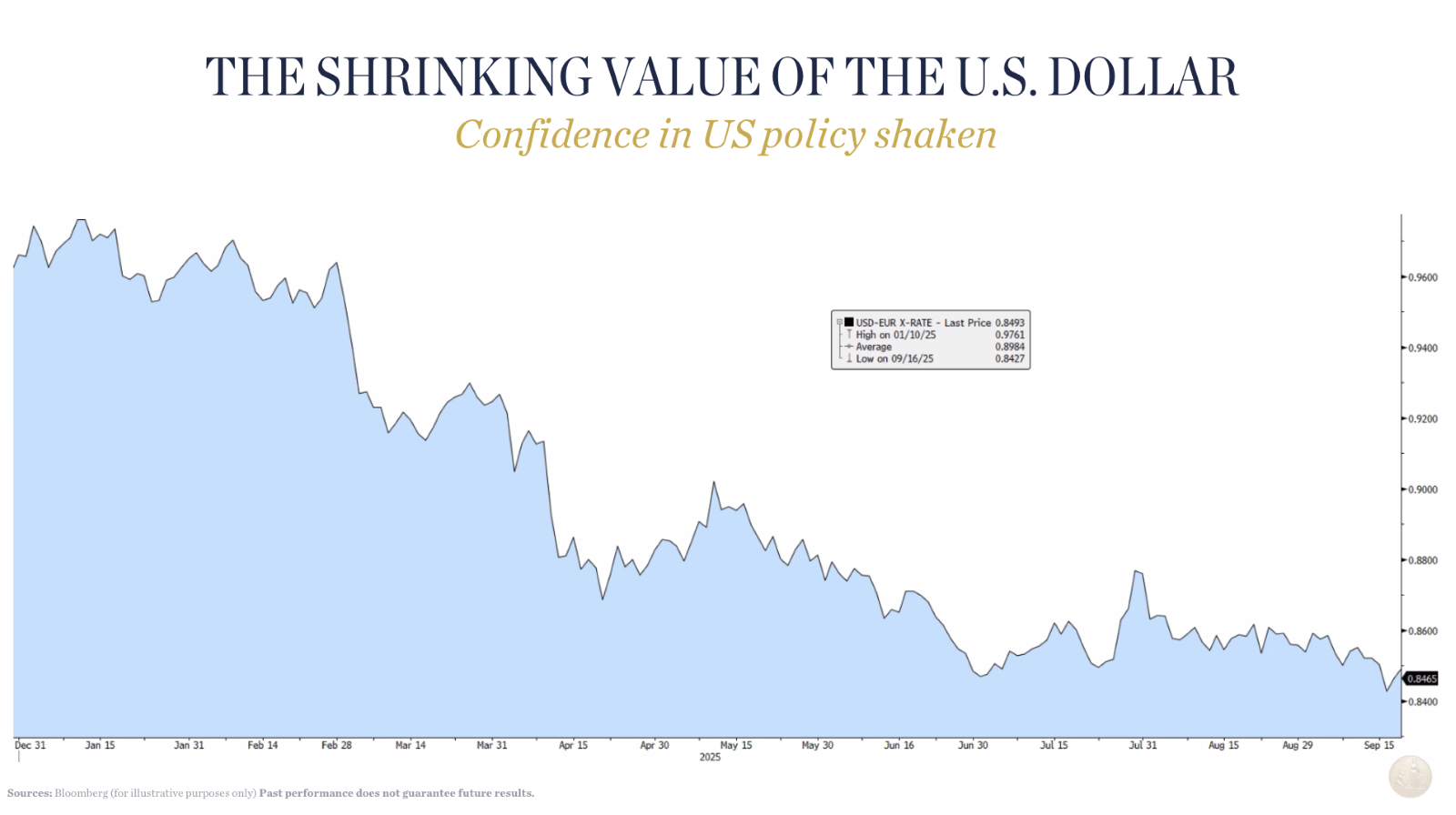

Why is the U.S. dollar weak, and is that normal?

The US dollar’s decline this year is the worst since 1981! This decline is tied to the significant changes due to the “New World Order” economic policy and the declining level of foreign confidence in the US as the most “exceptional” global economy. The Federal Reserve’s lower rate policy will likely create more headwinds for the value of the dollar. Since we are diversified in non-US-dollar-denominated foreign stocks, we are mitigating this risk.

How concerned should we be about the US deficit?

Many of these dramatic US economic policies are aimed at creating a more balanced budget and reducing debt. In many ways these are steps in the right direction, but only time will tell if they can remain consistently applied. We believe a US credit downgrade would pose a significant risk for global stock markets and we will be watching this closely.

What is the longevity of the AI bull market?

By many measures, we are still in the early phases of the AI revolution – but this needs to be closely monitored. Technological revolutions create massive capital investments, enhanced productivity and corporate profits, and send stocks soaring – all of which we have witnessed so far! However, these periods eventually lead to stock market bubbles, and once “popped,” the declines can be catastrophic – as we witnessed at the end of the infamous 1990s dot com bubble. We examine various metrics to track the progress of stock prices and valuations, keeping a sharp eye on the maturity of the AI stock bull market. One of the most important measures is the price-to-earnings ratio of each stock versus its growth rate. On this basis these stocks are not yet overvalued, and, in some cases, they are very reasonably priced. In the end – most likely more than a few years from now – it will end badly for investors as it always does. This eventuality is largely because investor psychology often gets the best of most investors, and they send stocks to unsustainable levels. We will monitor this risk as the AI bull market matures and continue to employ carefully placed stop-loss orders to mitigate greater-than-normal declines.

How can I protect my portfolio from risk of catastrophic decline?

We are bullish on certain US sectors, including AI technology, financials, and energy efficiency. We are also bullish on foreign stocks across most sectors. However, all this optimism can be misguided if there is a significant change in economic growth, central bank policy, or any number of unpredictable “black swan” events. For these reasons we always employ our Active Risk Management process, which incorporates the flexibility of reducing your stock exposure, changing it to more defensive sectors, and the use of carefully placed stop-loss orders. This process has mitigated significant losses in past bear markets, and we are confident that it will do so in the future.

If you have any questions about your portfolio or have experienced a significant change in your finances, please let us know.

From all of us – thank you for your continued vote of confidence in our work

If you have a family member, friend, or colleague who could benefit from our work or a no-cost wealth management and portfolio review, please let us know, and please feel free to share this Strategy Update.

Watch